vol. 13 no. 4, December, 2008

vol. 13 no. 4, December, 2008 | ||||

This exploratory study proposes a critical analysis of financial product design in order to better understand information seeking behaviour in the light of recent flawed financial product design. Indeed, the current international financial crisis, which began with the US sub-prime residential mortgages problem and has continued with a French derivatives products problem, reveals to us the problem of increasing financial sophistication. This situation should be carefully analysed and it causes us to question the information seeking and use behaviour for financial product development and about the information sources used. This information seeking and use behaviour will rely on specific information sources (economic, financial and marketing reports for example), and the choice of these information sources and the strategies used can explain the actual information seeking and use behaviour in financial product design.

To deal with this problem, we have developed a working hypothesis: 'The analysis of a user's "preferential information sources" can help us to understand their information seeking and use behaviour'. We will test this hypothesis within a specific theoretical framework, such as psycho-social theory, and demonstrate that this theoretical and methodological framework will help us to understand the process of information seeking and use behaviour. In our case, we need first to understand better the relationship between use of existing information sources by a financier and then to associate the sources with the financiers information seeking and use behaviour.

Thus, first, in our present analysis, after discussing the theoretical and methodological frameworks, we will present the psycho-social approaches and more particularly the social representation methodology we will use. Secondly, we will demonstrate our hypothesis with an exploratory study using one aspect of this framework, applied to the financial sector. Thirdly, we will show the result obtained by this approach and its limits, so as to understand better professional information seeking and use behaviour. Consequently, this study wishes to determine the information seeking and use steps for an engineering activity, and more specially financial engineering, within a specific framework and to show that we need more hybrid approaches if we wish to investigate this problem further.

According to Bates (2005), there are at least thirteen meta-theories or approaches that have been used more or less easily in information science:

But from our point of view, this overview of meta-theories is not complete. For example, some sociological approaches and psycho-sociological approaches are not present here. Moreover some relationships within approaches seem to be difficult to explain. According to Bates ( 2005), Vygotsky, Kelly, Dewey and even Garfinkel (ethno-methodology approach) use nearly the same 'constructivist' approach, but Vygotsky develops a more socio-cognitive approach than Kelly, who uses more psycho-cognitive approach. Also all the relationships between approaches are not very clear. As Bates (2005: 14) recognizes, 'each of the meta-theories above is part philosophy and some part methodology'. So we should use these frameworks cautiously in our own studies. Of course some approaches are not very easy to classify, such as the sense-making approach, although this could be considered as a socio-cognitive or an informational approach.

| Type of approaches | Approaches used by researchers | Authors cited |

|---|---|---|

| Ethno-methodology approaches | Grounded theory | B. Glaser. A. Strauss |

| Psycho-social approaches | Social representations | S. Moscovici, D. Jodelet, and W. Doise |

| Psycho-cognitive approaches | Personal construct | G. Kelly |

| Constructivism Information Science approach | Sense-making | B. Dervin |

| Sociological approaches | Socio-technical theory | E. Mumford, R. Bostrom |

| Actor network theory (sociology of translation) | B. Latour, Callon | |

| Socio-cognitive approach | Cultural-historical activity theory | L. Vygotsky, S. Rubinshtein, A. Luria, A. Leont'ev |

| Work centred framework | A. Pejtersen, R. Fidel |

If we look carefully at sense-making for example Tidline said, 'Sense-making is associated with a shift in research emphasis from information sources to information users' ( Tidline 2005: 113). This analysis is correct, but we should be aware that taking into account the information sources used can help us in our analysis of information seeking and use behaviour.

Researchers in the information science(s) field have used different theoretical and methodological frameworks for decades (see Kuhlthau (1996), Ellis (1993, 1997), Cheuk (1998), Fabritius (1998) and Hjörland (1997)), in order to understand information seeking and use behaviour and decompose the information seeking activity into several parts. But some theoretical frameworks are not generally used, although they are integrated in the constructivism paradigm. As Allen and Wilson (2003) note, 'Methodology is prior to method and more fundamental, it provides the philosophical groundwork for methods'.

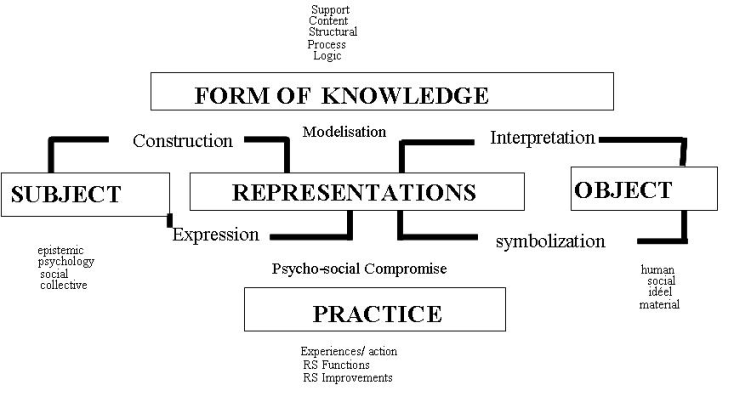

Social representation is a mental and perceptive elaboration process of the reality, which transforms social objects (persons, contexts, situations) into symbolic categories (values, beliefs, ideologies) and give them a cognitive status in our ordinary life. This allows us to focus on our own behaviour inside social interaction in order to understand all aspect of our ordinary life (see Piaget (2001), Moscovici (1976), Herzlich (1969), Jodelet (1984)). These social representations are pre-scientific knowledge, called 'common sense' knowledge. Representations are produced and become known in the collective culture. These social representation depend on language used, communication means (interpersonal, institutional and media) and society (social link, ideological context, social inscription and conceptual). As Jodelet said (1984), representation is practical knowledge, which helps a subject to conceptualize an object and to use it for future action, on the world and on others. Also, 'Une représentation est "générée collectivement" et "partagée par les individus d'un même groupe"' [A representation is generated collectively and shared by individuals of the same group.] (Jodelet 1991).

However, in our case and given the formulated hypothesis, the use of these notions supposes some limitations. That is why, even though we can not speak about social representations because the studied object concerns only a number limited of the population (essentially the asset management and marketing services), the financier's representation on this subject exist, because they are concerned by this crucial subject. Besides, methodologies developed by this current framework can be reused here. But we shall describe only representations shared with profession's members.

The elaboration of these representations begins with Thêmata, which can be defined as a set of first key ideas, archetypes, deeply embedded in the collective memory of a group. They allow one to emphasise what makes sense in this group. These Thêmata allow us to explain where the representations come from. Following this, for Moscovici and Vignaux (1994), thematic structuralization allows one to make objects relevant in the consciousness of this group.

Social representations, in this structural perspective, are elaborated and developed as a result of two additional cognitive processes, the objectivation and the ancrage (or anchoring). The objectivation process (Rouquette 1994) is a process of information simplification relative to the object and the 'anchoring process' is the social anchoring of the representation. It allows this representation to be attached to something already existing, which is shared by individuals belonging to the same group (Guimelli 1994).

Finally, according to Abric (1994), representations are organized with a central core and a peripheral system. The central core, corresponding to the stable part of the representation, is shared collectively by the group (Moliner 1994). The central core plays a structuring role by generating and by organizing representations. Then, the peripheral elements appear. They are closer to the real object but although they are dependent on the central core, they can also alter the central core. Abric (1994) summarizes the characteristics of the central system and the peripheral system of a representation: (see Table 2).

| Central system | Peripheral system |

|---|---|

| Linked to collective memory and group's history | Allow experiences accumulation and individual history |

| Consensus defines the homogeneity of the group | Supports group heterogeneity |

| Stable Coherent and rigid | Flexible Supports inconsistency |

| Stand up to change | Evolutionary |

| Less sensible to immediate context | Sensible to immediate context |

| Functions: Produce representation meaning. Specify his organization. | Functions: Allow adaptation to actual reality. Allow content differentiation. Protect central system. |

The objective of this research is to understand the information seeking and use behaviour of professional financiers and their relationship with information sources for financial product design. So we analyse the financiers' representation of this subject and try to find recurrent themes or key ideas that can influence their representations (central core and peripheral system).

Abric (1994: 78) advises us to use a multi-method approach. The collection of representations can be realized by methods, either inquiry methods (conversations, questionnaires, inductive boards, drawings and graphic supports, monographic approach), or associative methods (free association, associative cards). Afterwards, an analysis of classic resemblance will allow us to know the degree of structuralization of their representations (other methods can be used, such as the constitution of pairs of words or hierarchical organization of items). Finally, some techniques allow us to be sure of the centrality of the elements of the central system (questioning techniques, inductive methods by ambiguous scenarios, or the cognitive basic schemas method (Guimelli 1994: 83).

We use the analysis of resemblance approach (Flament 1994: 1995). In order to simplify, the resemblance analysis allows us to study different associations between lexical items that are part of the subjects' representation. This resemblance analysis is an indicator of the way a subject organizes representation for the design of the financial products.

We interviewed seventeen persons, in different levels of responsibility and in eight banks of different kinds mainly between 2000-2003. In order to know their representations, we use the constructivist paradigm and chose specific tools for our analysis already used as a part of the current trend of social representations (see Jodelet 1991).

A questionnaire was drafted which consisted of two parts: the first part of the questionnaire included fifteen open questions, which allowed us to verify the importance of information items used by the financial services, and to specify more precisely the searching and monitoring behaviour (as Bates defined in 2002) of financiers. The second part of the questionnaire (the most significant) uses the methodology of social representations in order to obtain a map of information items necessary for the design of financial products. This method describes representations shared among financiers and helps us to think about practices shared by the designers. However, we cannot use the term social representation because our sample size is too small, unlike Roussiau (1998) who worked on the representations of money with a bigger sample.

The first interest of this research is to better define the terminology used by the financial intermediary. We want to establish links between terms or information items and we want to obtain a terminological network's cartography. This global vision of items cartography in relation with others (by adding answers), allows us to obtain a collective and synchronic representation of the 'design of financial product' phenomenon, for the financial intermediaries. The main question is the following one: Where do the ideas come from in order to create a new financial product?

In this question, the financiers connect two categories of different items. On one side, we have the information sources: Official meetings, Financial press, Public general press, Market Studies, Confidential letters, Mailing & News Bulletin, Internal working groups, Internet and Personal contacts. On the other side, we have a group representing the deep-seated motives for designing a new financial product: Rules and laws, Fiscal policy, Competition, Customers satisfaction, Shareholders' demand, Economical Situation, Commercial, Bank profitability.

Every financier lists his preferences for different information items, and we can make the synthesis and obtain a collective lexical organization. Here are the various reserved items:

| Information sources | Motives |

|---|---|

| 1. Financial product design | 1. Fiscal policy |

| 2. General public press | 2. Market studies and marketing reports |

| 3. Confidential letters | 3. Rules and laws |

| 4. Official meetings | 4. Customers satisfaction |

| 5. Mailing and news bulletins | 5. Bank profitability |

| 6. Financial press | 6. Shareholders' demand |

| 7. Internal working groups | 7. Competition |

| 8. Personal contacts | 8. Economic situation |

| 9. Internet | 9. Salespersons |

In order to synthesize the links between these items, we employed resemblance analysis, using the APRIL software developed by CNRS (Silem et al. 1987: 127; Silem et al. 1984).

With this specific methodology and our sample, we can build a personal typology from the various information sources used by our financiers and we can obtain a more complete representation of every proposed item. Indeed, in this activity, two types of information dominate. There is the information for action and the information for constraint which oblige the designer to modify his design project, but which is bound to this design.

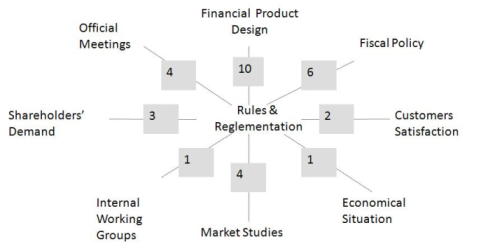

In this central system we find two different kind of central information: information for action, i.e.l information which allows us to act strategically (for example following customers needs, the competition or the shareholders' demand); and information for constraint, i.e., information which allows us not to commit malpractices as a rule or as a fiscal system.

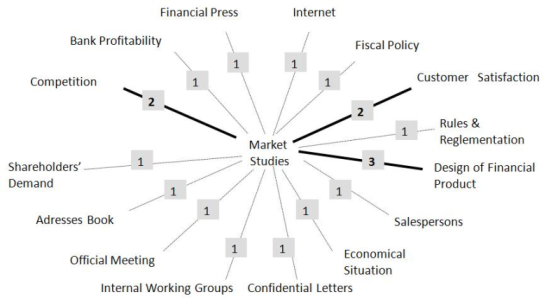

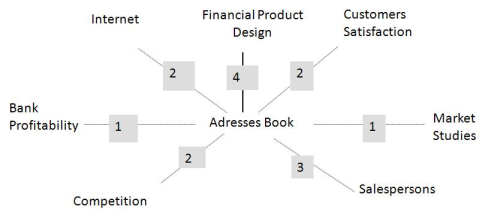

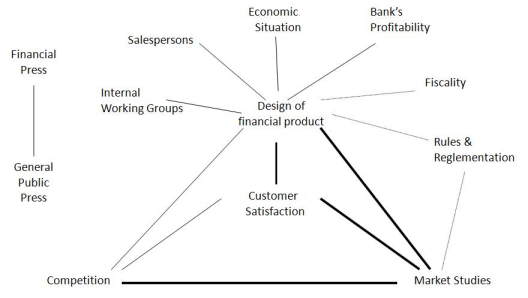

Marketing studies are key information for designers who want to make sure of the interest before introducing a new financial product. Moreover, the existence of very strong links between the item's Market studies and the item's Financial product design is demonstrated here (see below Figure 1). But other information, such as Customer satisfaction, is important also.

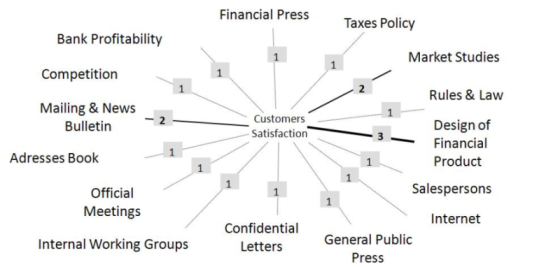

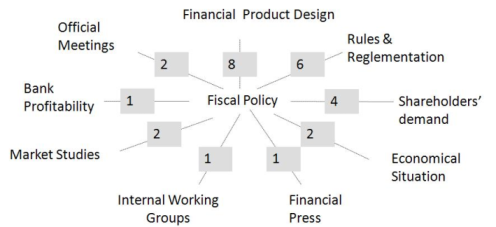

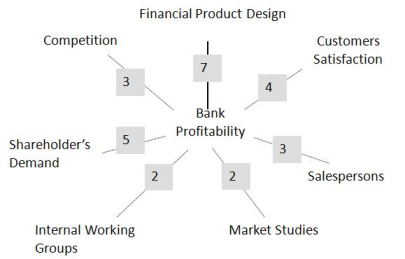

We should note that the link between items Customer satisfaction, Market studies and Financial product design are very close (see Figures 2 and 3). Fiscal policy should not be ignored for the financial product design (see Figures 4 and 5).

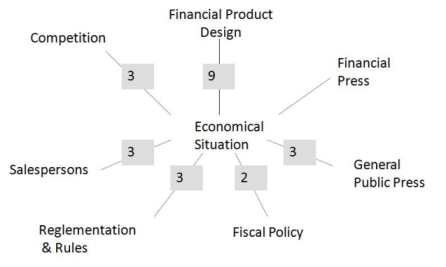

Competition and Economic situation should be taken into account too (see Figures 6 and 7).

This kind of information is important, but it does not always result from a direct and active search by the financier. This kind of information helps financiers to build new products in conjunction with other services of the establishment. We distinguish two kind of information, effective constraint information which blocks or changes the initial design project (for example internal working group, bank profitability and sellers), and the non-effective constraint information, which constitutes real challenges (documentation services, computer services, etc.). For example, new software should be developed in order to deal with these sophisticated financial products. Moreover, it's difficult to explain all the details of a new financial product (see the

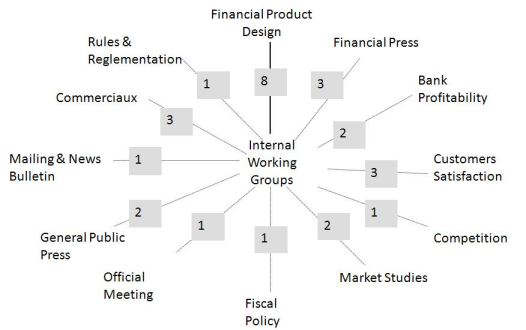

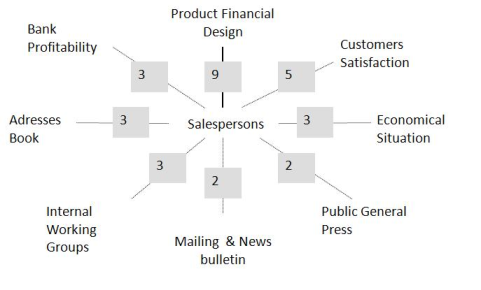

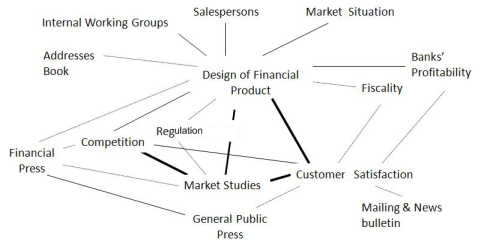

The design of a new financial product is a collective project and the Internal working group is essential for validating the design of the coquille (or shell) and the internal rules of the product (see Figure 8).

We should not neglect the financial factor (Bank profitability, see Figure 9) and the human factors (Salespersons, see Figure 10) which have an impact upon Financial product design.

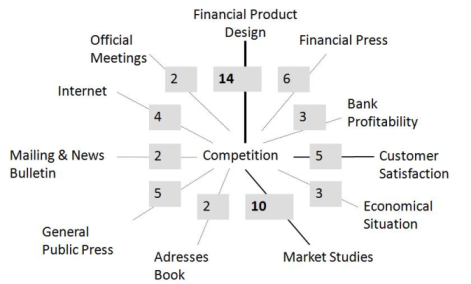

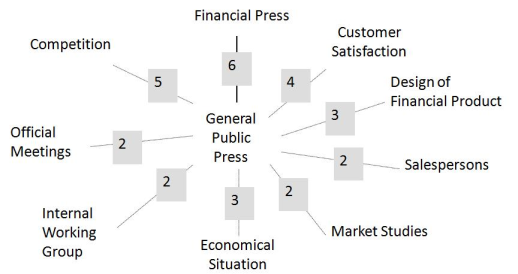

We observe that information sources are not used directly to create new financial products (the item Financial product design is not very often linked with other direct information sources). Only three information sources can be considered important: Market studies (already described above) which can be considered as an information source; General public press, which gives us a state of the world (see Figure 11) and Personal contacts, which show us the importance of interpersonal communication (see Figure 12).

This research underlines financiers' information priorities and choices. It allows us to extend our research into specific information sources that are dominant in the process of the design of financial products. By observing the results of this inquiry, we notice some interesting results, but these need to be augmented by further investigation.

This study shows us the importance of elaborated information, used for actions. We see the importance of using marketing information to bring about customer satisfaction, in order to conform to the new financial pulling and to respond to the actions of competitor. This information for action is directly balanced by constraining information such as commercial ideas, working group proposals inside the Bank or the Bank's profitability (see Figure 13). This constraining information is more or less taken into account.

If we continue our investigation, we discover the importance of the General public press and Personal contacts for financial product design (see Figure 14).

This graph shows us the importance of information resulting from networks (networks of commerce, of customers) and modern communication means (financial publications and the general public press).

This study also pushes aside traditional sources of information. They are not only the sources of financial or specialized information that dominate in the design of new financial products, but they are also the sources of non-specialized information and the marketing reports. Financial information is considered by the profession only as a mirror of itself and a light on the current situation in their daily lives. Moreover, we find that the oral or non-written documents play a more important role than the electronic document in the financial product design. For example how financial managers can explain sophisticated products such as collateralised mortgage obligations (CMO), collateralized debt obligations (CDO), collateralized synthetic obligations, CDO� (CDo of CDO), sometimes detailed with 100 pages of documentation, to sales and marketing persons and customers.

This study has the benefit of enlightening our understanding of this profession using a new perspective. Of course, this research was only exploratory and gives an outline of the reality at the moment, in a synchronous way, like a clich� (the phenomenon of the Internet modifies each information source and it has not been made particularly visible here). However, the work allows us to present the usefulness of the 'representations' concepts in the financial sector for designing financial products and services. It contributes to the analysis of this design process

In summary, this study shows us that this social-psychological approach can be used in order to understand information seeking and use behaviour and the information sources used. Even though our data sample was not significant, this methodology helps us to identify the separate information sources used by financiers. These information sources are distinctly different and indicate the diversity of search strategy. Inside the central system of the financier's representation, a direct and active search is used in order to find information for action and a more passive and undirected search is used for information for constraint (for definition see Bates 2002).

Thus, we have demonstrated our hypothesis, i.e., the deep analysis of professional and preferential information sources can help us to specify information seeking and use behaviour. Indeed, this study was interested mainly in studying how the designers of new financial products see their world and build new connections with information and, in a general way, how financiers think about the design of new financial products within their establishments.

Nevertheless as Henneron, Metzger, Palermiti and Polity said,

Dans le cas bien particulier d'un opérateur engagé dans une activité professionnelle, nous nous interrogeons sur la place qu'occupent les processus informationnels dans cette activité et sur la manière dont les acteurs s'informent. [In the specific case of a trader engaged in a business, we question the role of information processes in this activity and how players inform themselves.] (Henneron et al.1999: 13-14),

We should develop other frameworks in order to take into account the 'information which the user looks for and uses in his activity'. This study allows us to show the importance of elaborated information, (working group prefer to use their internal marketing report and customers' satisfaction survey )., but it does not allow us at this stage to model completely this search activity.

In order to model this complete activity, it would be necessary to determine more exactly professional representations for action, as well as the designers' deep motivations. It would also be necessary to analyse the socio-cognitive and informative process of design and decision, in order the better to understand reasoning, practices and steps of information seeking and use behaviour.

| Find other papers on this subject | ||

© the authors, 2008. Last updated: 7 December, 2008. |

|